Quarterly Market Newsletter – Q1 2026

NEWSLETTER | Q1 2026

A Quarter of Narrow Passages

Three straight years of strong market returns can do funny things to investor psychology. People stop asking whether the next leg up is earned and start assuming it is owed. Caution starts to feel like a tax. Then a quarter like this one comes along and resets expectations.

The story of Q1 was never about where the market ended the quarter. It was about what drove it there. Two very different forces collided over the past three months, and both are still very much in motion: a military conflict that rewrote the global energy conversation in a weekend, and a slower, stranger kind of anxiety inside the software industry over what artificial intelligence might do to a business model that has been remarkably lucrative for years. One arrived with sirens. The other built more quietly in the background. Both deserve our attention.

The War Nobody Priced In

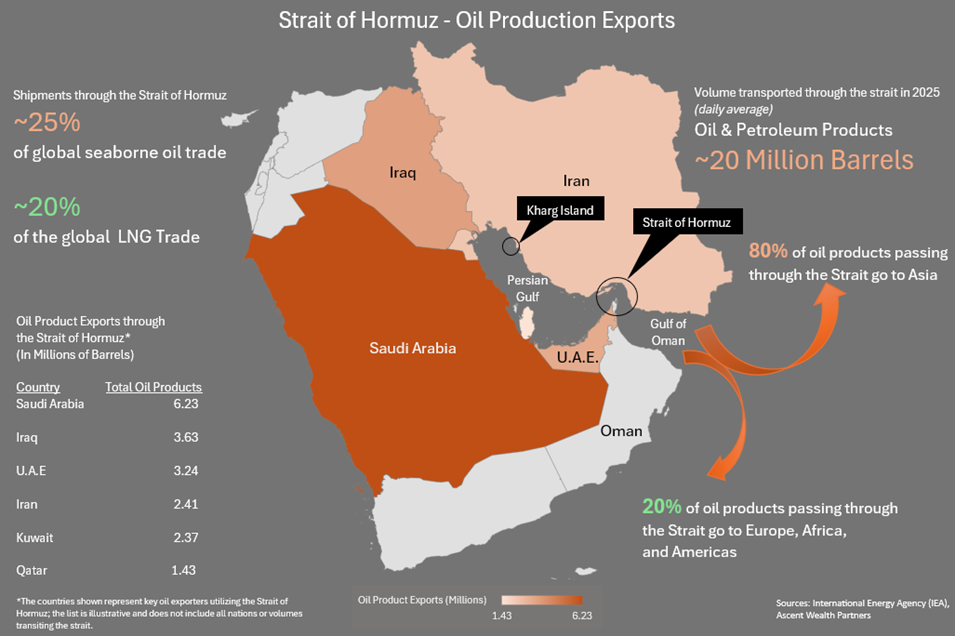

The defining event of the quarter, and possibly the year, was the military conflict with Iran. When U.S. and Israeli forces struck Iranian targets in late February, the market did not bother with nuance. It went straight to one thing: oil. And more specifically, one waterway.

The Strait of Hormuz is a narrow passage at the mouth of the Persian Gulf, and 20% – 25% of the world’s oil and natural gas pass through it every single day. That is an extraordinary concentration of global energy supply threading the eye of a needle that is twenty-one miles wide at its narrowest point, and it quickly became the pressure point of the entire conflict.

Iran did not need to formally blockade the strait. It only needed to make the passage frightening enough that shipping companies and their insurers refused to move tankers through. By March, more than two hundred oil tankers were sitting at anchor outside the strait, waiting for someone to tell them it was safe to sail again. Tanker traffic through the passage had effectively ground to a halt.

OPEC+, the alliance of oil-producing nations, responded the way it usually does when prices start climbing. It announced a production increase. Under normal conditions, that would help bring prices back down. But extra barrels are not particularly useful when there is no safe way to ship them anywhere. As long as the strait remains disrupted, any production increase is largely academic. And so prices climbed and stayed elevated for most of March.

Higher oil prices are not just an energy story. They are an everything story. Fertilizer prices surged within weeks, which is a problem that eventually shows up at the grocery store. Diesel costs work their way into trucking, manufacturing, construction and shipping. Anything that moves costs more to move. Anything that grows costs more to grow. When energy gets expensive, the bill eventually arrives at every door.

This is a particularly inconvenient moment for an oil shock. The Federal Reserve has spent the better part of four years dragging inflation back toward something resembling normal, and that work is not finished. An energy spike is exactly the kind of thing that complicates the job. For now, the economy still has enough momentum to absorb the hit. Consumer spending has held up, and the labor market, though cooling, is not cracking. Corporate balance sheets came into the year in reasonable shape. But there is a shelf life on that resilience. We are already more than a month into this thing. The longer it drags on, the more it stops being a headline and starts showing up as hiring decisions, earnings misses, and sticker shock at the pump.

A small disclaimer about reading any of these paragraphs too literally. This is a market trading on diplomacy almost as much as it is trading on fundamentals right now. Conditions could look very different by the time you are reading this than they did when we were writing it. What we do know is that geopolitical crises do not last forever. The White House appears to be increasingly looking for off-ramps, and the market is watching for any sign that ships are moving through the strait again. It is, for the moment, more a waiting game than a panic.

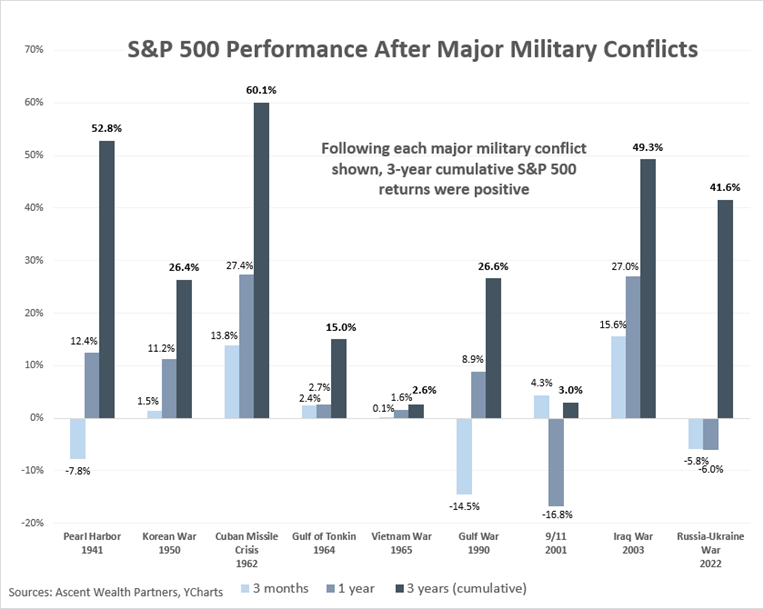

We are not pretending the risk has passed. If the conflict drags on, oil stays elevated, and higher costs start grinding through earnings and consumer demand, the pressure builds. We are watching that carefully. But history offers a useful anchor here: markets have recovered from every major military conflict of the past several decades, and usually sooner than anyone in the moment thought possible. That does not make the present any less uncomfortable. It just means the present is not the whole story.

When the Disruptor Gets Disrupted

The Iran conflict took up most of the oxygen in the room this quarter, but it was not the only story worth paying attention to. While everybody was watching oil, the technology sector was navigating a narrow passage of its own.

The traditional software industry had a rough Q1. That alone is news. For the better part of a decade, software was among the closest things the market had to a sure thing. These were beautiful companies on paper: asset-light, supported by recurring revenue, had customers who rarely left because switching was a nightmare, and blessed with profit margins that made other industries jealous. Wall Street loved them, and for a long time, that love was justified.

Then came the question nobody quite knew how to answer: what happens when artificial intelligence can do the work of several employees at once?

Here is the math that has been keeping software executives up at night. Most of these companies charge by the seat. One license per employee. If a single AI agent can replace five people in a customer’s office, that customer no longer needs five seats. Multiply that across thousands of customers and millions of seats, and the entire growth model starts to wobble. Many of these companies are still posting solid earnings. The selloff is not really about what they are today. It is about what the market thinks they will look like in five years, and when a stock has been priced for an almost uninterrupted future of growth, even a modest revision to that outlook can cause a significant repricing.

Our take is that the market is being a little indiscriminate about it. There is a meaningful difference between a software company selling a piece of generic productivity software and one that runs mission-critical operations for a Fortune 500 bank. The first is genuinely vulnerable. The second is much harder to dislodge, because compliance systems, security backbones, financial plumbing, supply chain operations do not get ripped out because somebody wrote a clever blog post about AI agents. Sorting one from the other is exactly the kind of work we are doing on your behalf.

What We Have Been Doing

We are not, by nature, frequent traders. Most of our work happens long before a crisis arrives. But periods of stress do tend to create opportunities, and when they do, we are willing to get more active.

There is no bell that rings at the bottom of a selloff. That luxury is simply not available to anyone. What we do believe is that when stock prices start drifting away from the actual quality of the underlying business, something interesting is happening. That is when we start looking more closely.

We came into the year with a slightly defensive lean, and that was intentional. After several years of strong returns led by the same handful of large technology names, we thought it was prudent to dial back risk at the margin. The clearest expression of that was an underweight to the more volatile and expensive corners of tech. When the software weakness started spreading in January, we went a step further and trimmed positions we believed were most exposed to the shifting economics of AI. Then we put that capital to work elsewhere.

The first place we shopped was on the energy side, after the events in Venezuela. We picked up a pair of Gulf Coast refiners built to process the heavier crude grades Venezuela produces, which puts them right at the doorstep of that supply if more of it returns to market. Refiners also make money on the spread between crude costs and refined product prices, which is a more targeted way to play the energy theme than a straight commodity bet on a producer

We also expanded on a theme we have been building for some time now: the physical infrastructure behind artificial intelligence. Most of the attention has gone to the chipmakers, and much of it is deserved. But AI runs on data centers, and data centers run on power, cooling, electrical equipment, and a long list of unsexy industry components that rarely make magazine covers. We are focused on the companies supplying the picks and shovels rather than the more speculative end of the trade.

Around the same time, we added to a leading streaming platform after it sold off on news that had little to do with the underlying health of its business. This is exactly the sort of dislocation we like. A strong long-term company gets temporarily marked down for reasons we do not believe change the bigger picture, and we get to buy more of something we already wanted to own. We will take that trade every time.

On the defense side, even before the Iran conflict, we initiated a position in the largest military U.S. military shipbuilder. That one was less about Iran and more about the steady drumbeat of military tension in the Pacific, particularly around China and Taiwan, and the simple recognition that the Navy is going to need more ships for a long time to come. It complements defense holdings we already had in place: a maker of missile defense systems, a builder of stealth aircraft and satellite platforms, and a provider of data analytics for intelligence agencies. As a group, those holdings give us exposure across the hardware, the platforms and the software brain behind defense spending.

The Bigger Picture

Difficult quarters can feel unsettling in real time. They almost always do. But they have a way of doing important work in the background, the kind of work that we can only really appreciate later.

For a few years now, market leadership had been getting narrower and narrower. A small handful of very large technology names were doing most of the lifting, and everything else had been fading into the background. This quarter was a useful reset. Areas of the market that had been overlooked for so long, including international and emerging market stocks, energy, and parts of the small- and mid-cap universe, finally started doing the job they are supposed to do. It is not always fun to live through. But it is healthy. And it is precisely the reason we build portfolios the way we do.

Earnings continue to grow. The economy, while clearly navigating some real headwinds, remains on reasonably solid ground. The fundamentals are not really what is shaking right now. The narrative is.

Our focus remains the same as it always is. Own quality. Stay diversified. Resist the urge to make dramatic decisions on the basis of headlines that may or may not look the same a week from now. The businesses we hold in your portfolios were not built for any single quarter. They were built to compound over years, and that has not changed. As always, please reach out with any questions. That is what we are here for.