Newsletter – Third Quarter 2023

2023 Rally Stalled in Q3

The momentum established at the start of the year extended into the early quarter. However, rising global bond yields, mounting concerns over rising inflation, and apprehensions regarding potential economic deceleration impacted the market as the quarter progressed.

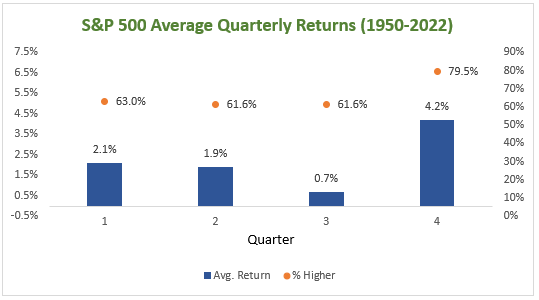

As we transition to the upcoming quarter, seasonality trends emerge for the better. Following a period of weaker performance in the third quarter, the market typically takes a more bullish turn in the fourth. Since 1950, the fourth quarter has been the most favorable for stocks, registering positive returns in nearly 80% of instances.

Source: Bloomberg. Past performance is no guarantee of future results

While historical data can provide perspective, it does not predict outcomes. The present market setup is complex: interest rates are at 16-year highs amid signs of growing consumer stress, especially among lower-income households. Rate-sensitive sectors such as housing and autos are weakening as higher borrowing costs for customers take their inevitable toll. Chaos reigns in Washington, and another government shutdown looms. As market participants continue to absorb the Fed’s message of “higher for longer” for the rate cycle, the S&P 500 has returned to its exceptionally narrow breadth, with a small handful of large stocks pulling the market average higher. Indeed, the index is negative on the year, when measured on an equal-weight basis.

Higher Interest Rates and National Debt

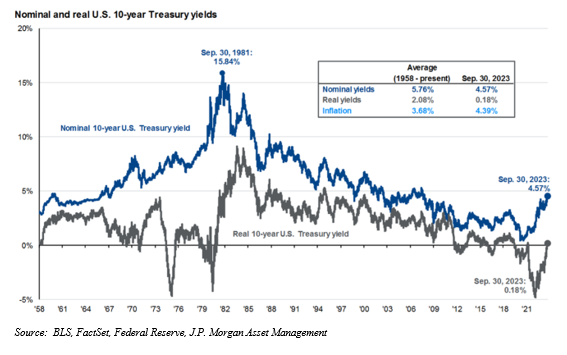

The recent surge in interest rates has significantly impacted financial markets. The yield on the 10-year Treasury hit a fresh multi-year high in the quarter, finishing at 4.57%. This increase in rates has been partially steered by a recalibration of expectations for upcoming Fed policy, coupled with concerns surrounding fiscal policy and the imbalances in sovereign debt supply. While these fiscal issues aren’t entirely new – the nonpartisan Congressional Budget Office (CBO) has issued warnings about the U.S. deficits and debt for years – recent developments have catapulted fiscal policy into the forefront of market discussions.

Source: BLS, FactSet, Federal Reserve, J.P. Morgan Asset Management

The federal government incurs a budget deficit when its expenses and investments outstrip its revenue, leading it to borrow money. Since its founding, the U.S. has always held some form of debt. For some historical context, in 1790 post the American Revolutionary War, the debt stood at over $75 million. For the next 45 years, this figure expanded, until 1835, when a combination of federally-owned land sales and budget cuts significantly reduced it. However, this respite was short-lived, as an ensuing economic depression once again elevated the debt. By the time the U.S. financed its role in World War I, the debt had grown substantially, standing at around $22 billion by the war’s end.

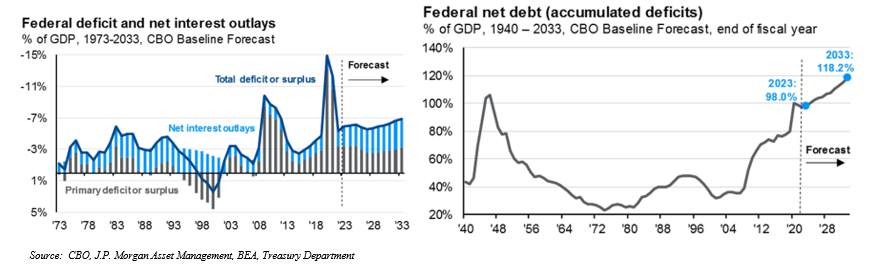

By the end of the U.S. 2023 fiscal year on September 30th, the national debt surpassed a historic $33 trillion. Recent events triggered large spikes in the debt. Between fiscal years 2019 and 2021, spending increased by about 50%, largely due to efforts to soften the economic blows brought about by the Covid-19 pandemic. Tax cuts, stimulus programs, increased government spending, and decreased tax revenue further drove government borrowing to record levels.

During the initial 11 months of the fiscal year (spanning from October 2022 to August 2023), the federal budget deficit reached $1.5 trillion, marking an increase of nearly $600 billion from the previous year. When viewed as a percentage of GDP, the deficit expanded from approximately 3.8% in the initial 11 months of 2022 to 5.7% in the current year. This comes after registering deficits of $3.1 trillion in fiscal year 2020 and $2.8 trillion in 2021. Projections for the forthcoming fiscal year anticipate a deficit surpassing $2 trillion.

Source: CBO, J.P. Morgan Asset Management, BEA, Treasury Department

The federal government incurs interest charges for borrowing money, much like an individual would for a car loan or mortgage. The interest amount the government pays is influenced by the total national debt and the respective interest rates on various securities. Over the past few decades, despite a consistent rise in the national debt, interest expenses have largely remained steady due to prevailing low interest rates. However, with recent rise in both interest rates and inflation, there is a corresponding uptick in interest expenses. According to Fiscal Data – a website established by the Treasury to consolidate federal financial data – as of August 2023, the cost to service our national debt stands at $808 billion, constituting 15% of the total federal expenditure. Furthermore, the CBO projects the average interest rate on U.S. debt will climb from the present 2.7% to 3.2% by 2033.

The rising federal deficit is at the forefront of debate in Washington, with lawmakers seeking to pass legislation ensuring government funding past September 30. A last-minute spending bill successfully staved off an imminent government shutdown, granting an extended 45-day window to finalize the funding legislation. Failure to reach a compromise to secure funding for the new fiscal year before the revised deadline could result in furloughs for hundreds of thousands of federal workers and halt various services.

U.S. Economy Resilient

Despite contending with headwinds that include persistent inflation and strict monetary conditions, the U.S. economy has continued to defy predictions of recession. From the latest estimate, U.S. economy grew at an annualized rate of 2.1% in the second quarter of 2023, only marginally below the upwardly revised first quarter’s expansion of 2.2%. The Atlanta Fed GDPNow’s forecast for the third quarter now anticipates real GDP growth to accelerate to 4.9%, suggesting a continuation of the strong growth trend.

From the September employment update, payrolls saw a significant boost with an addition of 336,000 jobs. This marks the 33rd consecutive month of job growth. Over the course of the year, the U.S. has seen an addition of over 23 million jobs to its economy. The current unemployment rate is nearing a half-century low, contradicting many economists’ predictions that rising interest rates would lead to widespread layoffs.

Beyond our borders, China is confronting challenges in its overextended real estate sector, marked by significant debt and an abundance of unsold apartments. At present, few are expecting falling real estate prices in China will lead to a cascade of major bank collapses, reminiscent of the 2008 financial crisis in the U.S. A key distinction is China’s banking landscape; the government holds significant stakes, either directly or indirectly, in nearly all banks, ensuring considerable sway over their fate, beyond its already formidable regulatory authority. Although U.S. and European banks face limited direct exposure to China’s troubled real estate market, this downturn underscores the pressing need on policymakers to shore up growth in the world’s second largest economy, which is stalling after an initially strong post-Covid rebound.

Our Outlook

While 2023 has largely been favorable for investors, the horizon presents notable uncertainties. Central to our concerns is the sharp rise in Treasury yields. Since summer, the yield on the 10-year Treasury note, pivotal for many loan benchmarks, has steadily climbed, prompting corresponding hikes in various borrowing rates. The costs of servicing mortgages, auto loans and credit card debt have all risen in its wake. The jump in longer-term rates compounded by external challenges: escalating energy prices, the resumption of student loan payments, the ongoing autoworkers’ strike, and the possibility of a government shutdown. Collectively, these factors risk curtailing consumer spending, a vital engine of our economy.

Current projections suggest a modest rise in corporate earnings for 2023 when compared to 2022. After three straight quarters of year-over-year declines, a firmer recovery in earnings appears to be on the horizon as we approach the year’s end. This momentum is expected to pave the way for a more pronounced growth as we look ahead to 2024.

As we assess the various challenges impacting both the economy and the stock market, a degree of near-term apprehension is undoubtedly valid. Yet, we must not overlook the time-tested resilience of the equity market as a steadfast ally for long-term investors. Time and again, the equity market has demonstrated its capacity to rise above temporary disruptions, presenting long-term rewards for those with patience and fortitude. At Ascent, our dedicated investment team stands firm in its commitment to navigate through these evolving challenges, ensuring our clients’ interests are always at the forefront.